Overton Window to the Wall | Why the Debt to GDP ratio is broken and what it takes to secure our economic future

Photo Credit: ChatGPT

By Brett Seaton

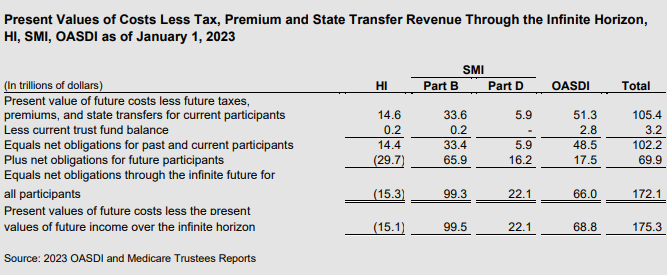

The United States is 35 trillion in debt. But this actually paints a rosier picture than the Treasury Department’s most recent report which estimates the total deficit at 175.3 trillion.

Yet, no one seems to care. The reason for our apathy is that the previous sentence was absolutely meaningless. All we hear when we read 35 trillion and 175 trillion is “a lot” and “a lot a lot”, respectively. What if I said that this equates to $530,000 per person? Again this suffers from a reference point problem–why can’t we push it up to $1,000,000 per person?

Large numbers sound like monopoly money if we do not ground the conversation in terms of relative indebtedness. This is critical because it is how debt investors evaluate which governments to give money to and which to not. In turn, the opinions of debt investors are critical because countries do not go bankrupt because they hit X amount of debt, they go bankrupt because debt investors refuse to invest in them, so they can no longer pay back prior debtors.

Debt divided by GDP is usually used as a proxy for relative indebtedness between countries. The benefit of this measure is that it pegs the amount of debt a country can take on to the size of that country’s economy. In the private market, debt is pegged to earnings before interest, taxes, depreciation, and amortization (EBITDA) which is usually somewhere between 10% – 30% of revenues. In the US, the average EBITDA margin is about 13%, which would give $3.7tn of EBITDA on last year’s GDP. If you then apply a relatively high leverage ratio of 5x, the US economy’s debt capacity is around $18.7tn (note this does not include household level debt or government level debt). Since the US government debt is $175tn, we are about 47x levered and 42x over-levered today.

This analysis, however, severely misses the mark because it compares apples to oranges. GDP is thought of as the “revenue” of a country, and yet Government revenue (read: taxes) is always a percentage of GDP, and usually a low percentage. At the same time, all of the government’s debt is attributable to the Government, not to the American economy. So, the revenue number is significantly inflated. The maximum percentage of GDP ever captured by the government in forced taxation was in 1951 when tax receipts as a percentage of GDP hit 17%. This rate has steadily declined since then, and today is around 10%. We should incorporate this information in our measurement of indebtedness and use Debt / Government Revenue, because it includes tax rates which are a function of critical market dynamics. The United States can tax more than some countries, because of the dynamism of our economy, the stability of our democracy, and the rule of law that we have built, but we cannot escape the global trend towards tax reduction.

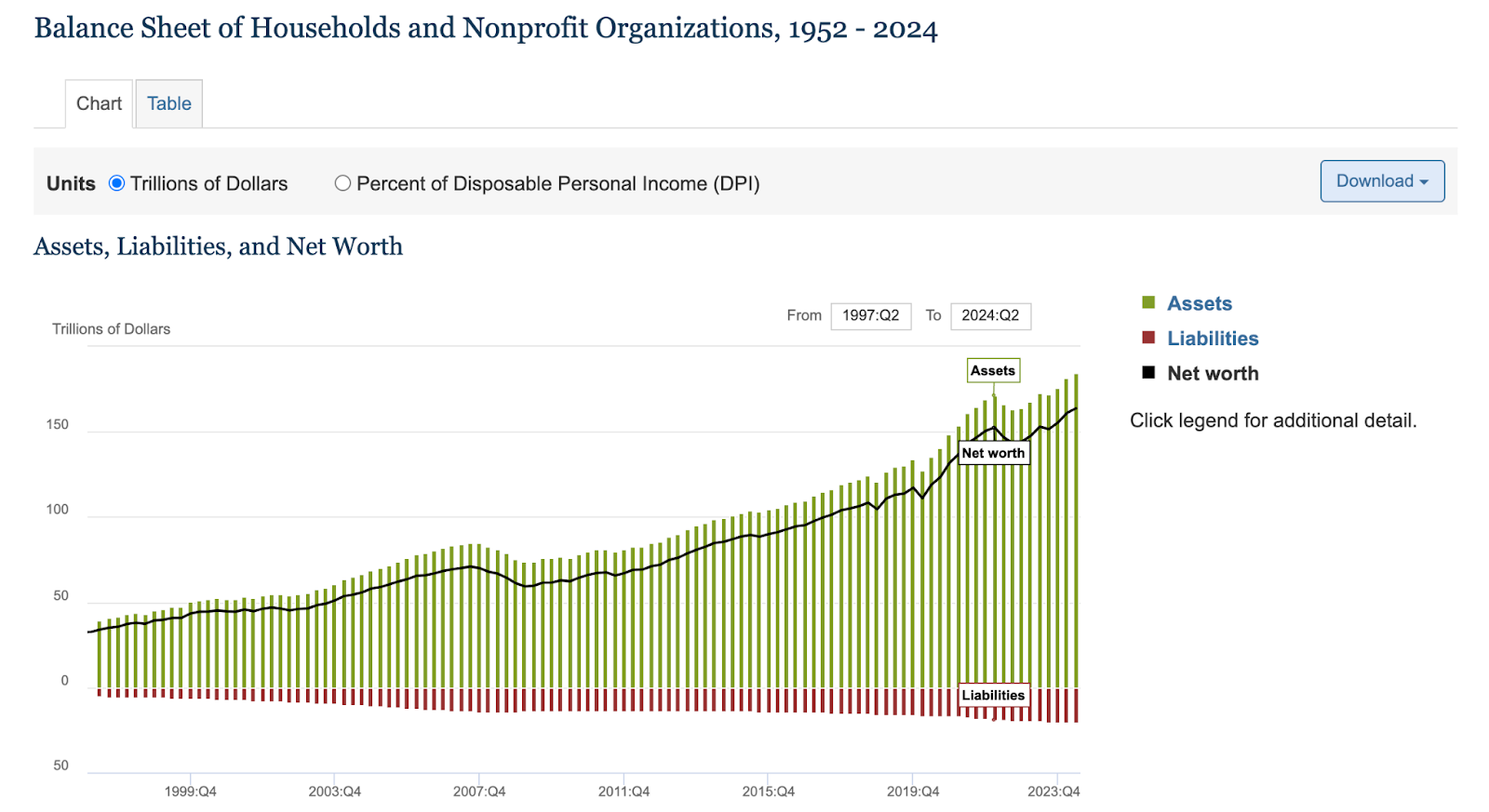

Macroeconomic talking heads reference the Debt / GDP ratio as if it was handed down by the central banking gods of yore despite it cross-pollinating two fundamentally different entities–the United States economy and the United States Government. This metric’s biblical status reveals a horrific premise of its proponents–that the United States economy and the private wealth therein is obtainable through forcible theft. Proponents of this metric will point to the below graph and say, “Lo, you silly doomsdayer, we do not have a debt issue!”

But, if you take a closer look at that graph, you will notice that these are household assets, not Government assets. The Government viewing private assets as collateral against their federal credit card is not only incorrect because wealth will flee if the Government begins to seize it, but also conceptually head-spinning in that it confuses representation with ownership.

Let’s end the confusion. The Government is not the economy. It is a company whose revenue is forced taxation. The company’s relative indebtedness is a function of its revenue, its costs, and its debt burden–not the GDP of the country that this company is in. Its customers are citizens who consciously decide to live here and pay higher taxes than they would pay in other countries. This “business” has grown expenses 0.8% faster than revenue since 1950. This business is at least 47x over-levered, and the cost of just its employees, medicare, and social security are greater than its revenue today. If this business continues to operate as-is it will implode under the weight of its debt and global competitive disadvantages. Would you give this business your money when you could give it to Apple or any other better business instead?

In the long run, the answer is no. Investors saying no to the company will bring bankruptcy and economic Armageddon for all its stakeholders (American citizens).

The business has one option to avoid this—it must cut costs. It must cut the budget by 27% to no longer be adding to the debt. It doesn’t matter how we do this–we can cut any combination of expenditures to get there–but there will be consequences to each cut. I made a game in excel called Game of our Lifetime which you can download from this google drive link that helps you understand how many cuts we need to make and what these consequences are.

If President Trump wins the upcoming election, this will be the game that Elon Musk plays, should the Department of Governmental Efficiency (DOGE) he has proposed be effectuated. If Vice President Harris wins, she or her successor will be forced to play the same game. Go play and help the American business survive the game of our lifetime.

Brett Seaton is a senior in Wharton studying Finance from Manhattan, KS. Brett is also the Ombudsman for The Pennsylvania Post. His email is bseaton@wharton.upenn.edu.