Franchetti’s Facts | Despite major buzz, publicly listed private credit vehicles are exhibiting signs of strain.

By Abraham Franchetti

One of the most important financial trends of the past few years has been the rise of private credit. Between 2009 and 2023, the private credit market has grown by roughly ten times to more than two trillion dollars. These markets have become a favorite for investors and debtors alike due to fast deal turnarounds at large volumes. However, like any other asset class, the influx of cash has the risk of creating a bubble. Due to the creation of publicly traded vehicles, typically in the form of business development companies (BDC), a broader set of investors are exposed to these risks, and some data on these private loans is available. This includes data on income collected as Paid in Kind (PIK) interest, which indicates when a company is given the option to pay its interest as a lump sum with the debt principal. This limited pool of data suggests that some private credit BDCs are displaying signs of stress, and further inquiry to their safety is necessary. Overall, private credit BDCs are exposing their public market investors to unrecognized risk due to tactics to increase volumes on safe loans and failures to mark valuations.

Some of the features that make private credit more attractive than bank loans are the same factors that drive unique risks. First, private credit is attractive because it can be issued faster than syndicated loans. This single issuer element, which provides speed, also creates risk by ensuring that company-specific risk is not diversified by a variety of firms. Second, private credit firms are more willing to finance larger loan volumes than banks. This can be accomplished by using the same leverage multiples as a bank, but by being more lenient regarding EBIDTA add backs. These adjustments often do not reflect tangible business environments and high debt loads create added risk. Private credit is also much less liquid than syndicated debt. Rather than being underwritten and traded by a variety of firms, this debt is usually held by a single or small group of issuers. This results in assets which are rarely traded and thus “marked to model”. As a result, markets are far less efficient or effective at pricing private credit loans. These factors combine to make some private credit portfolios both risky and opaque.

A key case study for these flaws occurred with Vista Equity’s $3.5b investment in Pluralsight. The debt which Vista used to acquire the company used “covenants based on recurring revenue” in order to achieve even higher volume than adjusted EBITDA multiples would allow. This was only possible in private credit markets because “we’re likely still a long way from seeing these loans pass the sniff test for ratings agencies (a requirement for a true syndicated solution)”. As the COVID tech boom transitioned into a contracting market, Pluralsight suffered. Despite Vista’s efforts, the company’s situation continued to decline, with Vista marking down equity value from $2.3b to $0 over the course of a year.

Pluralsight was turned over to creditors in summer 2024, led by Oaktree, Blue Owl, and Blackrock. The handoff will reduce debt by $1.3b and enable the investment of $250m in new money. Overall, Pluralsight is the tip of the spear in private credit backed firms in distress. The extreme leverage based on revenue projections, paired with a significant decline in their sector, led to the company’s rapid collapse. Pluralsight’s creditors now have possession of a company which has already lost more than half of its valuation, and will likely see further decline. This equity position is a major shift from a credit position, requiring sector expertise to direct the company, eliminating the set exit timeline, and reducing liquidity and exit options. After losing billions of dollars in value, new management will attempt to turn it around, and some of its creditors including Oaktree Global Opportunities have extensive experience in this. However, if situations like this become common, it could lead to a broad deterioration. When functional companies become over burdened with debt and enter bankruptcy this disruption reduces efficiency and economic activity.

Challenges in marking debt are evident in the Pluralsight case. As early as Q1 2023, Vista asked creditors to loosen loan agreements. Yet in June of 2023, the valuation among creditors ranged from 100% to 95%. Only by March of 2024 did companies substantially re-evaluate, with valuations ranging from 97% to 84%. By June, valuations experienced a more than 40% decline, now ranging between 50% and 46%. The company was subsequently handed over to its creditors. Whether or not this is a failure to accurately reflect the true value of the company rather than a rapid deterioration is up for debate. Regardless, it seems clear that when private credit firms are faced with relatively minor challenges such as needing to loosen covenants (which covenants were loosened has not been disclosed), they are not making changes to their valuations that anticipate future deterioration. Using the valuations on BDC balance sheets may not be accurate for this reason, and other leading indicators must be sought.

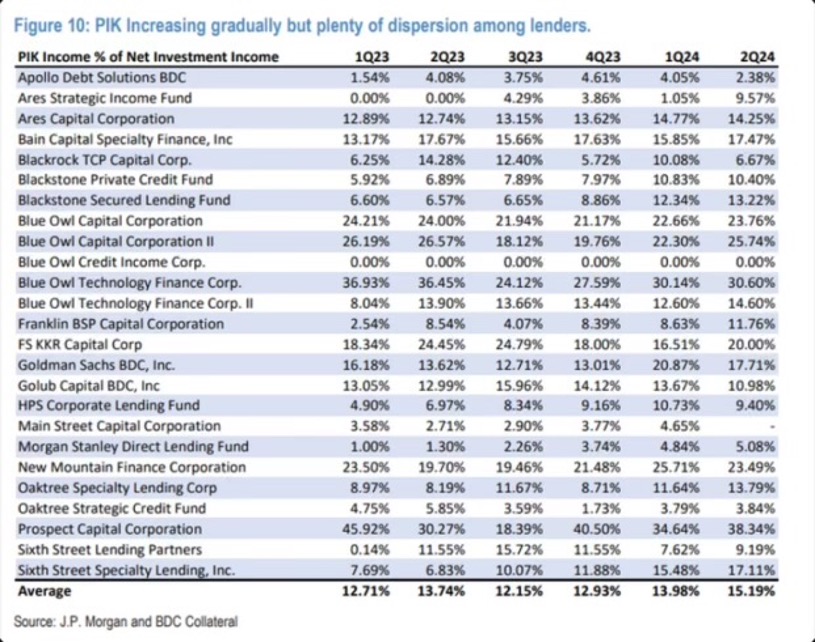

One way to examine the extent of risk in BDC portfolios is using its percentage of PIK income. When their debtors are unable to meet interest payments, private credit firms will engage with them to ensure a smooth process for both parties. The most common form of this is by allowing PIK (paid-in-kind) interest. Rather than requiring debtors to pay interest now, interest expenses are added to the debt principal. This is mutually beneficial: companies get short term relief and private credit firms can avoid the public exposure and questioning from a larger scale restructuring. As a result, receiving PIK interest is a viable proxy for assessing whether a private credit firm’s debt holding is risking distress. Based on data from JPM and BDC Collateral, there are several private credit lenders whose portfolios’ consist of a large amount of PIK income payments. 38% of Prospect Capital and 30% of Blue Owl Technology Finance Corp’s (OTIC) net investment income is in the form of PIK interest.

Despite this, OTIC’s Q2 2024 shareholder report advertises a 0.0% loss rate, and does not mention PIK interest at all. Blue Owl Capital Corporation, which had offered debt to Pluralsight, collects 23% of net investment income as PIK. Despite this, they have only written down two investments: Pluralsight’s senior secured debt and CIBT Global’s senior secured loans (OBDC 10-Q Q2 2024). OBDC has 212 portfolio companies, 82% of investments are senior secured. High rates of PIK interest collection in a senior secured position across hundreds of portfolio companies indicate a level of instability that is not being reflected in valuations on Blue Owl’s balance sheet. This problem is widespread. Bloomberg reports that analytics firm Solve found that “three quarters of PIK loans were valued at more than 95 cents on the dollar at the end of September.” These high levels of PIK collection indicate that among some of the largest funds, more than 20% of their portfolio is unable to service its interest.

The emergence of “synthetic PIK” further complicates this assessment. Synthetic PIK refers to a new practice where new debt is offered by a private credit firm to meet interest payments on old debt. This tactic enables debtors to appear as if they are paying their interest while in reality being unable to meet those obligations. Bloomberg reports that private credit firms are using this tactic specifically because their facilities from banks can include “a cap on the share of PIKs in the portfolio, which helps guard against an excess of lower-quality credits”. Using synthetic PIK to avoid breaching covenants with banks or appearing unstable is one more example of how these single issue lenders are skirting responsibility and admission of bad debt. This is harmful for investors because this new debt can have the same level of security as the primary facility but may emerge from a different private credit firm vehicle, diluting BDC investor claims.

Overall, analysis of the current market for private debt exposes major weaknesses for BDC investors. Using aggressive add-backs or alternative multiples that ratings agencies wouldn’t approve, sponsors and creditors have overburdened companies with debt. Because mark to model valuations can have massive swings, it is difficult to trust the presented loan values in BDCs. Moreover, the substantial percentage of income being reported as PIK suggests widespread strain on these portfolios – which are not reflected by valuations. When assets that are considered safe are experiencing undisclosed strain, investors with a low risk appetite or investing knowledge are put at risk. One way to ameliorate this problem is for investors and regulators to step up rating and disclosure requirements for these public vehicles. However, these actions will not fix assets that are already distressed, and could lead to a reduction in BDC valuations as well as concerns about private credit issuers.

Abraham Franchetti is a junior in Wharton studying Finance with a minor in Classical Studies from Port Washington, NY. Abraham is also the Business Director for The Pennsylvania Post. His email is bramf@wharton.upenn.edu.